Bookkeeping for Small Business Owners: Beginner’s Guide 2026

A

admin

•

June 7, 2026

•

11 min read

•

0 Comments

Bookkeeping is the foundation of every financially healthy business. Without it, you have no clear picture of what your business earns, spends, or owes — and tax season becomes a stressful scramble through receipts and bank statements.

The good news is that bookkeeping for small business does not have to be complicated. With the right system in place, most small business owners can manage their books in just a few hours per month.

This beginner’s guide walks you through everything you need to know about small business bookkeeping in 2026 — what it is, how to set it up, which records to keep, and how to stay IRS-ready all year long.

What Is Bookkeeping?

Bookkeeping is the process of recording, organizing, and tracking all financial transactions in your business. Every time money comes in or goes out — a sale, an expense, a loan payment, a payroll run — that transaction gets recorded in your books.

Good bookkeeping gives you:

A clear picture of your business profitability

Accurate records for tax filing

Data to make smarter financial decisions

Protection in the event of an IRS audit

The ability to get business loans or attract investors

Bookkeeping is often confused with accounting. The difference is straightforward — bookkeeping is the daily recording of transactions, while accounting is the interpretation and analysis of that data. Most small business owners handle their own bookkeeping and hire an accountant for tax preparation.

Bookkeeping vs Accounting: Key Difference

Task

Bookkeeping

Accounting

Record transactions

✅ Yes

✅ Yes

Categorize expenses

✅ Yes

✅ Yes

Reconcile bank accounts

✅ Yes

✅ Yes

Prepare financial statements

Partial

✅ Yes

File taxes

❌ No

✅ Yes

Financial analysis & strategy

❌ No

✅ Yes

Cost

Lower

Higher

Step 1 — Choose Your Bookkeeping Method

Before setting up your books, you need to choose a bookkeeping method. There are two options:

Cash Basis Accounting

You record income when you receive payment and record expenses when you pay them. This is the most common method for small businesses and freelancers because it is simple and reflects your actual cash flow.

Best for: Sole proprietors, freelancers, and small businesses with annual revenue under $25 million.

Accrual Basis Accounting

You record income when it is earned (even if not yet received) and expenses when they are incurred (even if not yet paid). This gives a more accurate long-term picture of your business finances but requires more complex record-keeping.

Best for: Businesses with inventory, large receivables, or revenues over $25 million (required by IRS above this threshold).

Recommendation for beginners: Start with cash basis accounting. It is simpler, easier to manage, and works for the vast majority of small businesses.

Step 2 — Open a Separate Business Bank Account

This is the single most important bookkeeping step many small business owners skip — and it causes massive headaches at tax time.

Open a dedicated business checking account and use it exclusively for business transactions. Never mix personal and business expenses in the same account.

Why this matters:

Separates your personal and business finances completely

Makes categorizing transactions fast and accurate

Protects you in the event of an IRS audit

Required if you operate as an LLC or corporation (commingling funds can pierce the corporate veil)

Makes bookkeeping take minutes instead of hours

Also consider opening a separate business savings account where you set aside 25–30% of every payment received for estimated taxes. For more on managing quarterly tax payments, visit Finance Ledger Tips.

Step 3 — Set Up Your Chart of Accounts

A chart of accounts is a categorized list of every type of financial transaction your business makes. Think of it as the filing system for your books. Every transaction you record gets assigned to one of these categories.

Standard Chart of Accounts for Small Business

Assets (what your business owns)

Cash and bank accounts

Accounts receivable (money owed to you)

Inventory

Equipment and property

Liabilities (what your business owes)

Accounts payable (bills you owe)

Credit card balances

Business loans

Payroll liabilities

Equity (owner’s stake)

Owner’s equity / retained earnings

Owner’s draw or distributions

Income (money coming in)

Sales revenue

Service revenue

Other income

Expenses (money going out)

Rent and utilities

Payroll and contractor payments

Office supplies

Marketing and advertising

Software subscriptions

Travel and mileage

Meals (50% deductible)

Professional services (accountant, attorney)

Insurance

Equipment and depreciation

Most bookkeeping software comes with a pre-built chart of accounts you can customize for your business type.

Step 4 — Choose Your Bookkeeping System

There are three main options for managing your books:

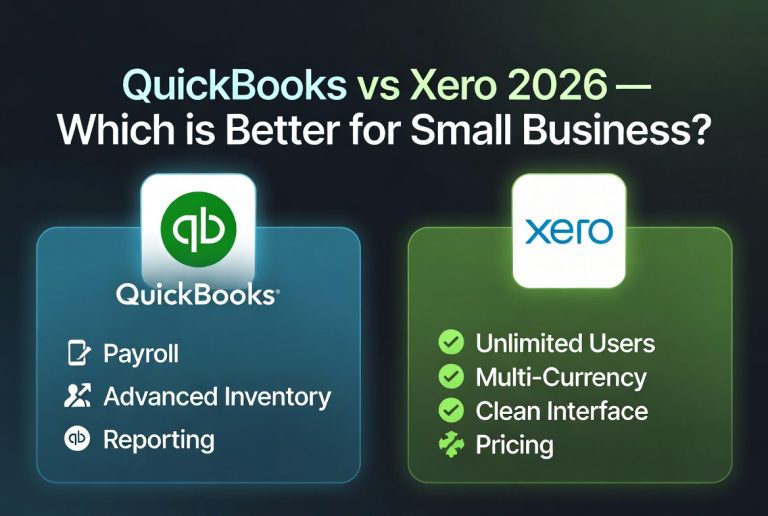

Option 1: Bookkeeping Software (Recommended)

Software automates transaction imports, categorization, bank reconciliation, and financial reporting. The top options in 2026:

QuickBooks Online — Most widely used, strongest reporting, best accountant compatibility. Starting at $35/month.

Xero — Clean interface, unlimited users on all plans, great for growing teams. Starting at $15/month.

Wave — Free accounting software ideal for solopreneurs and micro businesses.

FreshBooks — Best for service businesses that invoice clients regularly.

For a full comparison of accounting software options, visit Finance Ledger Tips.

Option 2: Spreadsheets

Google Sheets or Excel can work for very simple businesses with minimal transactions. Download a free bookkeeping template, record every transaction manually, and reconcile monthly. This works for freelancers with under 50 transactions per month but quickly becomes unmanageable as your business grows.

Option 3: Hire a Bookkeeper

A professional bookkeeper typically charges $300–$800/month for small business bookkeeping, depending on transaction volume. This makes sense once your business grows beyond what you can comfortably manage yourself, or if accounting is simply not your strength.

Step 5 — Record Every Transaction

The core of bookkeeping is simple: record every financial transaction in your books as it happens. This includes:

Income transactions:

Every invoice paid by a client

Every sale made through your store or platform

Deposits, interest, and refunds received

Expense transactions:

Every bill paid (rent, utilities, subscriptions)

Every business purchase (supplies, equipment, software)

Every contractor or employee payment

Every business meal, travel cost, or mileage expense

The golden rule: If money moves in or out of your business bank account or business credit card, it goes in your books — categorized correctly, with the date and a brief description.

Step 6 — Reconcile Your Bank Accounts Monthly

Bank reconciliation means comparing your bookkeeping records against your actual bank and credit card statements to make sure they match. Every transaction in your books should match a transaction on your bank statement.

Why reconciliation matters:

Catches data entry errors before they compound

Identifies missing transactions

Detects unauthorized charges or fraud

Ensures your financial reports are accurate

Most bookkeeping software connects directly to your bank and imports transactions automatically, making reconciliation a quick monthly review rather than a manual process.

How to reconcile:

Download your bank statement for the month

In your bookkeeping software, open the reconciliation tool

Match each bank transaction to a recorded transaction in your books

Investigate and resolve any discrepancies

Mark the reconciliation complete

Aim to reconcile every account — checking, savings, and every business credit card — at the end of each month.

Step 7 — Track and Categorize Business Expenses

Accurate expense categorization is critical for two reasons — it gives you an accurate profit picture and it ensures you claim every deduction you are entitled to at tax time.

Your bookkeeping system should produce three core financial reports every month. These reports tell you the financial story of your business.

1. Profit and Loss Statement (P&L)

Also called an income statement, this shows your total revenue, total expenses, and net profit or loss for a given period.

Revenue − Expenses = Net Profit (or Loss)

Review your P&L monthly to spot trends, identify overspending, and measure growth.

2. Balance Sheet

The balance sheet shows your business’s financial position at a single point in time — what you own (assets), what you owe (liabilities), and your net worth (equity).

Assets = Liabilities + Equity

3. Cash Flow Statement

The cash flow statement tracks the actual movement of cash in and out of your business. A business can show a profit on its P&L but still run out of cash — the cash flow statement shows why.

Most bookkeeping software generates all three reports in seconds. Review them at the end of every month and before any major business decision.

Step 9 — Keep Your Records and Receipts

The IRS requires you to keep business records for a minimum of 3 years from the date you file the return they relate to. Some records must be kept longer:

Record Type

How Long to Keep

Tax returns

At least 7 years

Bank statements

7 years

Receipts for deductions

3–7 years

Employment tax records

4 years

Business asset records

Life of asset + 7 years

Contracts and agreements

7 years after expiration

Best practice: Scan and digitally store all receipts using an app like Dext, Hubdoc, or your bookkeeping software’s built-in receipt capture. Paper receipts fade and get lost — digital copies are more reliable and easier to retrieve.

Step 10 — Prepare for Tax Season Year-Round

The biggest bookkeeping mistake small business owners make is neglecting their books for 11 months and then scrambling in March. When your books are current, tax season is straightforward.

Monthly bookkeeping routine:

Record all income and expenses

Reconcile bank and credit card accounts

Review profit and loss statement

Set aside 25–30% of net income for taxes

Quarterly tasks:

Calculate and pay quarterly estimated taxes

Review your year-to-date financial reports

Update your mileage log

Review and adjust your budget

Annual tasks (January–February):

Issue 1099-NEC forms to contractors paid $2,000+ in 2026

Collect W-2s from employees

Provide your accountant with year-end financial statements

Keeping accurate books also protects you from IRS scrutiny. Common red flags include:

Claiming 100% business use of a vehicle — very rarely accepted without detailed mileage logs

Excessive meal and entertainment deductions — meals are only 50% deductible

Large home office deductions relative to income

Inconsistent income reporting — revenue on bank statements that does not match reported income

Rounding all numbers — exact record-keeping looks more credible than rounded figures

Best Bookkeeping Software for Small Business 2026

Software

Best For

Starting Price

QuickBooks Online

Most small businesses

$35/month

Xero

Multi-user teams

$15/month

Wave

Solopreneurs / free option

Free

FreshBooks

Service businesses

$19/month

Zoho Books

Growing businesses

$20/month

Frequently Asked Questions

Q: How often should I do bookkeeping? Ideally, record transactions weekly and reconcile accounts monthly. Letting bookkeeping pile up makes it significantly harder and more error-prone. Set aside 1–2 hours every Friday to update your books.

Q: Do I need an accountant if I do my own bookkeeping? Yes — even if you manage your own day-to-day bookkeeping, hiring an accountant for year-end tax preparation and quarterly reviews is worth the investment. They will catch deductions you missed and ensure your returns are filed correctly.

Q: Can I do bookkeeping myself with no accounting background? Absolutely. Modern bookkeeping software is designed for non-accountants. With cash basis bookkeeping and a solid software tool, most small business owners can manage their own books with minimal training.

Q: What is the difference between single-entry and double-entry bookkeeping? Single-entry bookkeeping records each transaction once (like a checkbook register). Double-entry bookkeeping records each transaction twice — as a debit in one account and a credit in another. Most bookkeeping software uses double-entry automatically, even if it does not look like it to the user.

Q: How do I handle cash transactions in bookkeeping? Record every cash transaction in your books on the day it occurs, just as you would a bank transaction. Keep a cash log if you regularly receive or spend cash, and reconcile it against your records monthly.

Final Thoughts

Good bookkeeping does not require an accounting degree — it requires consistency. Record every transaction, reconcile every month, review your reports regularly, and keep your records organized. Do those four things and your books will always be ready for tax season, a business loan application, or an IRS inquiry.

Start simple: open a business bank account, choose a bookkeeping software, and spend 30 minutes this week getting your chart of accounts set up. That one hour of setup will save you dozens of hours every tax season.

For more guides on bookkeeping, payroll, taxes, and accounting software for small business, visit Finance Ledger Tips.

Leave a Reply